Vlad Kochetov

Quantitative Developer & Researcher

Exploring academic literature, implementing cutting-edge methodologies, and solving complex problems at the intersection of machine learning and quantitative finance.

About Me

Quantitative researcher and developer focused on systematic trading and market structure. Experienced in building execution systems, simulation environments, and machine learning pipelines for data-driven strategy development.

Projects

FPGAEnv

GRPO environment for training LLMs to write synthesizable Verilog, graded via Verilator simulation. Parameter-free scoring based on clock-cycle ratio to handwritten references. Reward hacking prevented through per-episode randomized vectors, Verilog syscall guard, and sandboxed execution.

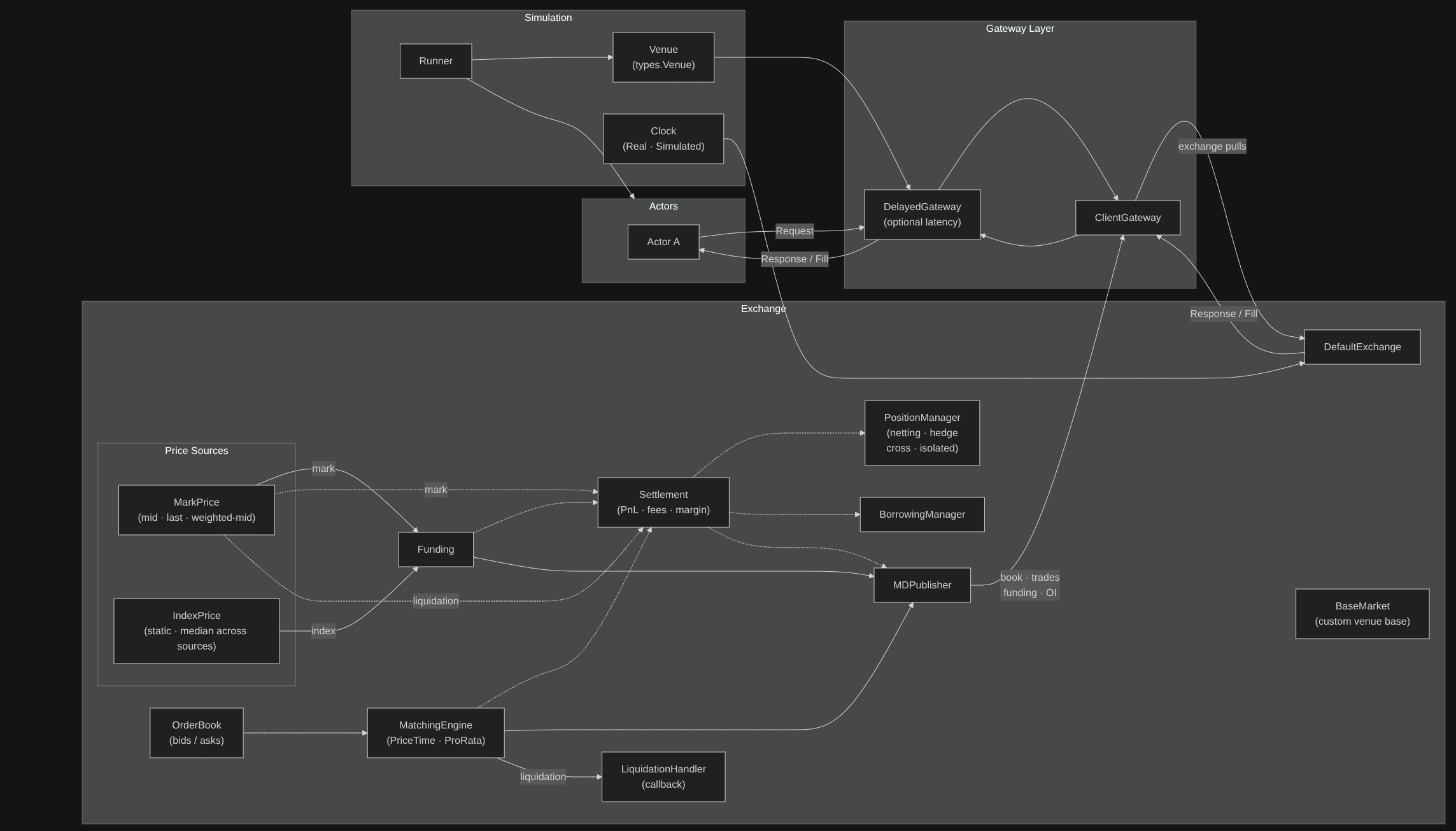

Exchange Simulation

Actor-based exchange simulation with a full order book, Price-Time & Pro-Rata matching engines, and realistic mechanics: mark price, liquidations, insurance fund, and circuit breakers.

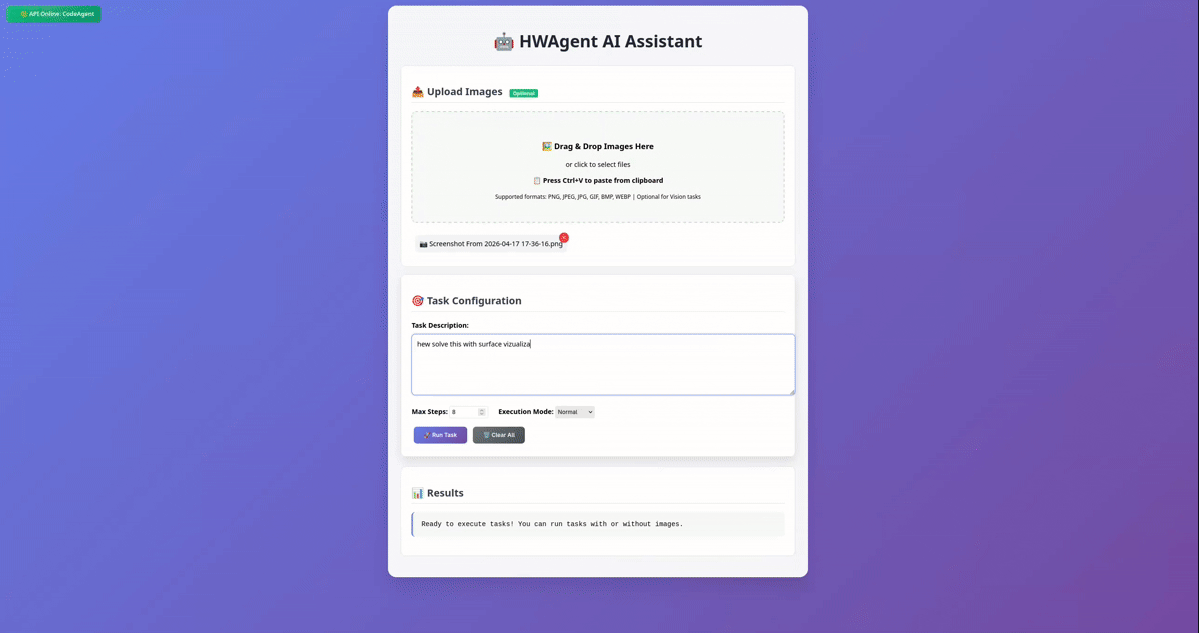

HWAgent

First hands-on experience building agents. Built on top of smolagents when cheap LLMs still struggled with complex math reasoning. LLM output goes to executable Python parsing, code execution loop, result verification, step-by-step LaTeX solutions, automated matplotlib plots, and PDF export. Goal: guaranteed correctness instead of hallucinations.

Get in Touch

Always open to interesting conversations, opportunities, and collaborations.